In January of 2009, a major car manufacturer announced a novel “Assurance” program which was designed to reduce the risk to consumers of taking on new debt during what has been dubbed “The Great Recession.” If the buyer became unemployed or disabled, went bankrupt, or accidentally died within a year of purchasing her shiny new crossover vehicle or his sporty coupe, he or she could return the car to the dealer and (metaphorically) walk away from any financial obligations with no further penalties. In crafting this program, the company cleverly homed in on the two essential elements of middle-class mentalité. On the one hand, consumption serves as a critical indicator of both current class status and confidence in one’s future; the economic and social aspirations of the middle class are best demonstrated by what one owns. On the other hand, the assumption of additional debt might easily undermine a middle-class existence dependent on the continuation of a regular income. Particularly during hard times, the fear of potential failure and loss of status causes the middle class to become extremely risk averse. The consumptive impulse (the devil on your left shoulder telling you to “buy! buy! buy!”) is now replaced by the contrasting virtues of frugality and self-restraint (the angel on your right shoulder telling you to “save! save! save!”). Hoping to clip the angel’s wings, this “Assurance” program aimed to remove the risks associated with conspicuous consumption, allowing middle-class consumers to focus on their aspirations rather than their fears.

While the crossover vehicles of the early American republic relied on a slightly more literal understanding of “horse power” and “air conditioning,” two hundred years of industrial progress has nevertheless left the competing elements of this mentalité virtually unchanged. Then, as now, this self-described class optimistically assumed that economic mobility was always possible, that talent and hard work would be recognized, that modest comforts in the present were the just rewards of such previous efforts, and that the ability to secure an even better economic future for one’s children was the ultimate payoff. Yet, while prosperous times encouraged this optimism, economic downturns revealed the fragility of such beliefs. As historians such as Edward Balleisen, Bruce Mann, and Scott Sandage have revealed, the potential for profit and prosperity needed to be carefully balanced against the perils of engagement with the marketplace. As Americans moved from agricultural regions into burgeoning, anonymous cities, as families became dependent on the cash income of the head of the household rather than a more holistic family economy, and as businessmen became aware that their economic fortunes were as much dependent on the booms and busts of the business cycle as on their own abilities, the long-term economic fate of middle-class families became increasingly uncertain and fraught with anxiety.

Most studies of the nineteenth-century middle class in America have focused on providing a group portrait, correctly emphasizing that it cannot solely be defined by income level. Rather, one must also consider their social and cultural conduct, including their movement into salaried, non-manual occupations, their embrace of reform movements, their assertion of control over family size, their segregation of public and private sectors in and outside the home, and their consumption patterns. Yet this group portrait neglects to explain how the middle class reacted to economic shocks. What did they actuallydo when facing hard times? How did they preserve their aspirations for the future—a critical element of their status—when facing economic struggles in the present? It is only when middle-class hopes and fears meet the realities of a modern economy that a fuller picture of its experiences can emerge.

Edward Balleisen addresses these questions in Navigating Failure, where he examines the actions of several hundred middle-class bankrupts during the 1840s and concludes that the desire to mitigate risk was the key lesson taken from their experience. While many embraced the risks inherent in the market by seeking to re-establish themselves as independent small proprietors after their initial failure, they now adopted a much more cautious approach in their commercial reincarnation by seeking to limit their use of credit and avoid the high risks (and thus high returns) of more speculative opportunities. Other bankrupts adopted a more extreme response, either rejecting the market outright by embracing a communal lifestyle in one of the many utopian communities of the period, or by seeking to reproduce the landed independence of previous generations in becoming a farmer out West (with or without market aspirations).

Many more sought a compromise between these two extremes: limiting their exposure to market risk by redefining ideal middle-class vocations. The economic independence of self-employment, once valued as the definitive attribute of a middling competence, was now re-conceptualized to signify an occupation that bound the proprietor in a life-long struggle with credit and debt, raising questions about the ostensible “independence” that position conferred. In contrast, salaried occupations were now reconceived as providing personal independence even as they reduced the once self-employed man to the role of employee. As Balleisen concludes, these risk-averse individuals “redefined autonomy in terms of security and freedom from the anxieties that so often beset the owners of business ventures.”

While hard times often occurred as the result of macroeconomic shocks that resulted in widespread suffering—such as the Panic of 1819 or 1837, the Great Depression, or our current “Great Recession”—individual families might also fall on hard times independent of the booms and busts of the business cycle. In particular, the death of the main breadwinner quickly exposed the precariousness of middle-class status. Remedies such as the short-lived Bankruptcy Act of 1841 were designed to cushion the impact of business failure by enabling many American debtors to break free from their overwhelming debts and start their economic lives anew. Yet even this solution left families vulnerable if the head of the household died. What if death intervened before the bankruptcy proceedings were completed, or before the person was able to reestablish himself in business? As one observer concluded in 1837, “The late and present pecuniary embarrassments of the mercantile world, and the consequent derangement in every thing connected with it, … show conclusively the necessity of making provision for dependents that shall be beyond the control of reverses in trade or commerce.” In particular, this provision needed to take into account the possibility of death, “a contingency which, when it happens is irremediable—beyond which no recovery of disastrous step can be made.” Whereas the negative economic impact of death had always been present, panics and depressions served to underscore middle-class fears of failure and socio-economic decline. “With these turns in the business cycle,” Mary Ryan contends in Womanhood in America, “many a loyal wife watched her economic security disintegrate in some financial wizardry that she scarcely understood.”

The negative impact of death was only compounded as urbanization removed the economic and social safety nets that had existed in rural societies. Several options were available for widowed and orphaned families in the countryside. Under the common law of dower, widows received a fixed share of the real property owned by their husbands; under the law of most states they received lifetime use of one-third of the husband’s landed property. Fatherless households could thus continue running the family economy in his absence—particularly when older sons were available to help on the farm or continue his trade. The assistance of family and neighbors was vital to this transition, while children and paid farmhands provided long-term stability. Even families lacking the economic, emotional, or human capital necessary to continue without a husband and father were not left out in the cold. Neighbors and relatives readily incorporated victims of loss into their own household economies. Historian Jack Larkin has pointed out that “the chances for early death made for many widows and widowers who frequently found places in the households of their children or of their married brothers and sisters. Kinfolk came into their relatives’ families as paid or unpaid domestic help, apprentices and employees, and even paying lodgers.” The very nature of the household economy in agrarian America helped to shield families from sudden economic dislocations when the family head died.

The situation for urban families was much different. While a solvent businessman could rest assured that his firm would provide for his family after his demise, either through continuance by another family member or by a profitable liquidation, the salaried man could take no such consolation since his money-earning power died with him. The transition of the home from a place of production (with responsibilities divided among all family members) to one exclusively of consumption put considerably more pressure on the role of the primary male breadwinner, who knew that the family could not survive without his income. Families who lost their fathers and husbands faced a dismal fate because the wages paid to women were not designed to support their survivors, and a decline in class status necessarily ensued. For many, then, remarriage—and a return to the dependent confines of the private sphere—was the only means of maintaining their middle-class status.

Nineteenth-century fathers similarly experienced increasing expectations to establish middle-class foundations for their children. Whereas the offspring of previous generations were likely to follow directly in the footsteps of their parents, a father now needed to ensure adequate education and training, if not capital investments, for his son’s future career. His daughter, as well, needed to acquire the appropriate literary and musical skills to be considered marriageable. For many fathers, the ability to provide a proper education for their children became both symbolic of their success as a middle-class parent and a critical sign of their continued class status. Yet a father’s untimely demise might force his children to enter the workforce prematurely, sacrificing the education that was increasingly critical to middle-class life.

Support from family or neighbors was much more limited in the cities as well. Urban residents were not heartless, but interpersonal obligations and connections were fluid in this highly mobile environment. Whereas taking in the needy in rural communities added productive units to the household, at least partially compensating for their additional consumption, they became extra mouths to feed in the city—placing undue strain on household budgets. In the mushrooming towns and cities of antebellum America, the plight of the widowed and the orphaned thus emerged as a new concern, particularly as the waged piecework women could take home was not designed to guarantee survival.

During the early nineteenth century several charitable organizations such as the Society for the Relief of Poor Widows with Small Children, the New York Female Guardian Society, the Association for the Relief of Respectable or Aged Females, and the Association for Improving the Condition of the Poor were founded in order to provide aid for the “deserving” poor—among whom were included (according to the 1852 report of the latter) “females once in comfortable circumstances who have been reduced to poverty by the death or misfortune of their husbands and relatives.” While these charitable organizations certainly performed a crucial function for nineteenth-century Americans in need, however, no moderate-income father wanted his family to become “dependent upon the cold charities of the world” after his demise. He found it “indispensably necessary,” rather, “that some sure and unfailing provision should be made to those who are dear to him, a sufficient competency to place them beyond a miserable dependence upon public charity after his death.” Indeed, even though most charities targeted those considered most deserving, the idea of receiving charity remained stigmatized and many widows who aspired to protect their middle-class status refused such handouts.

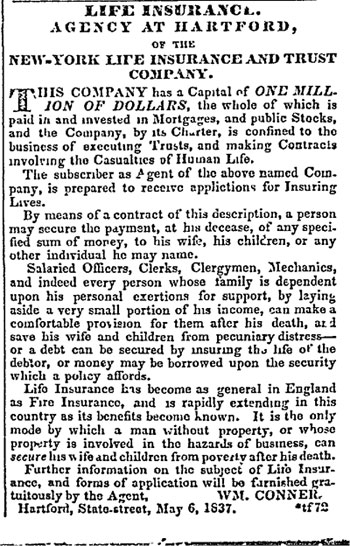

To avoid subjecting one’s family to such a horrifying potential fate, middle-class fathers increasingly sought out the protection offered by the emerging life insurance industry. Starting in the 1810s and 1820s with the chartering of the Pennsylvania Company for Insurances on Lives and Granting Annuities and the Massachusetts Hospital Life Insurance Company, and then rapidly growing in popularity during the 1830s with the New York Life Insurance and Trust Company and the Baltimore Life Insurance Company, life insurance promised to maintain the economic wellbeing of a family after a breadwinner’s death. In particular, the industry understood that the growing urban middle class faced opportunities and anxieties that made them unique among Americans. As an 1858 New York Life Company brochure proclaimed, life insurance appealed not to their status consciousness—as people “who imagine themselves rich in this world’s goods”—but to their recognition of the fragility of that same status. By providing not just “a certainty against future want” but also the “comforts of life” for families (a contemporary concept signifying the consumables that marked a family’s class status), life insurance offered a hedge against the economic vicissitudes of middle-class life. As is evident in the marketing literature produced by the industry, all antebellum life insurance companies believed that their most lucrative business would come from fathers whose death would leave their families in “pecuniary distress,” “in want,” in a state of “poverty, in the hour of their distress,” suffering “sacrifice and loss,” or exposing them “to insult and poverty” or “the horrors of destitution, of want, and of misery.”

Reflecting the most basic anxieties of middle-class Americans, these bleak descriptions resonated throughout urban society. Letters to Baltimore Life from potential policyholders have survived, providing a rare (albeit brief) glimpse at people’s motives for insuring themselves during the 1830s. One lawyer from Sanford, Virginia sought a $3,000 policy “to insure a living to my wife” while another Virginian, in anticipation of making a marriage proposal, wanted “to secure to a Lady if she shall survive me, $10,000, if not then to my children.” A Richmond, Virginia, businessman—who would later become Baltimore Life’s local agent in that city—explained: “It has since occurred to me that having a Family of young Children dependent in a great measure on my exertions it would be a matter of prudence to effect a Life Ins[uranc]e. Say to the am[oun]t of $3000 for their benefit.”

Merchants and small proprietors, in particular, were well aware of the high rate of business failure in America, and thus sought insurance to protect their families against the risks inherent in their source of livelihood. “I have been raised to the mercantile business, and think I have the capacity and opportunity to employ capital advantageously,” explained one entrepreneur from Memphis, Tennessee, in 1845. “And in obtaining it,” he continued, “would be very glad to avail myself at the same time of the protection afforded by such an Institution as yours, against the vicissitudes of trade, and the sufferings to a young and helpless family which might result from my death in a state of poverty.” Middle-class inquirers sought life insurance in order to secure the economic future of their families, thus freeing them to pursue their professional aspirations with less fear of the consequences of failure.

Due to its location near the nation’s capital, Baltimore Life targeted its sales among Washington’s growing military and bureaucratic workforce. When the company officially opened a Washington agency in March of 1833, its new agent’s main objective was to sell insurance policies to government clerks. In his acceptance letter, this agent declared that he was “located in the midst of the public offices, & have an intimate acquaintance with nearly all the officers of the Departments, a class of persons of all others the best suited to the object of your Company,” due to their status as salaried professionals. As with the emerging pockets of “white-collar” workers throughout the eastern seaboard, he viewed these federal employees—many of whom were likely young clerks with higher professional aspirations—as a prime target for the life insurance industry. In an 1839 letter to the company president, the agent stressed that “Many of the clerks are notoriously improvident, most of them receive inadequate Salaries; and very many leave their families at their death in a most deplorable State of destitution.” These clerks lived on the cusp of middle-class existence. While their non-manual employment and long-term aspirations placed them firmly within a middle-classmentalité, their modest incomes left them particularly vulnerable to losing that precarious social status.

By midcentury, insurance advertisements increasingly reached beyond mere allusions to poverty or sacrifice and fully embraced the emotional turmoil that was by now a central part of middle-class life. A blatant example of this type of psychological marketing tactic is found in the 1848 brochure of the New York branch of Eagle Life Insurance Company of London. The firm painted a picture of one thousand young healthy males who dreamed of marrying and passing on their middle-class status as “successful independent operatives” to their offspring. During their lifetimes these men would easily be able to support their families in a comfortable, even refined, existence, yet Eagle Life estimated that half would die an early death: “the children of five hundred are doomed in some way, to eat the bread of dependency. There is no effort of ordinary economy which can save them from such a contingency,” which would leave them “a hunger-driven herd of shiftless individuals.”

The concluding paragraph of this description brought home the nightmare scenario dreaded by every self-respecting modern patriarch—that his children would fall out of the middle class and have to repeat the struggle up the ladder of their father and grandfather. Upon premature death, “his heirs and representatives must instantly descend many grades in the scale of comfort, if not of respectability; to feed on husks and breathe in corners, and find in scattered places, and among varied chances a vague hope of attaining in after years a snug hearthstone like their father’s.” These advertisements thus rehearsed a classic dictum by which the sins of the father (failing to adequately protect his family through life insurance) became a yoke borne by his children.

Distinct from the social obligations of rural society and the pity of urban charities, a life insurance policy was a breadwinner’s best investment in his family’s future. Indeed, this was a novel market solution to a pressing market problem. The growth of insurance over the course of the nineteenth century paralleled the development of a middle-class mentalité by providing a new safety-net to protect middle-class widows and orphans from a loss of class status, by facilitating the aspirations and lifestyle they sought in the present and by allowing them to continue educating their children for advancement up the socio-economic ladder in the future. It freed the middle class to take more risks during their lifetimes since their wives and children would now be protected from the risks of death in a modern economy.

Further reading

References to life insurance company brochures are found in Historic Corporate Reports, Baker Library Historical Collections, Harvard Business School. Correspondence with insuring customers is from the Baltimore Life Insurance Collection, MS 175, H. Furlong Baldwin Library, Maryland Historical Society.

For general studies of the nineteenth-century middle class, see Cindy Sondik Aron, Ladies and Gentlemen of the Civil Service (New York, 1987), Stuart M. Blumin, The Emergence of the Middle Class: Social Experience in the American City, 1760-1900 (New York, 1989), T. Walter Herbert, Dearest Beloved: The Hawthornes and the Making of the Middle-Class Family (Berkeley, 1995), Paul E. Johnson, A Shopkeeper’s Millennium: Society and Revivals in Rochester, New York, 1815—1837 (New York, 1978), or Mary P. Ryan, Cradle of the Middle Class: The Family in Oneida County, New York, 1790-1865 (Cambridge, 1981).

For studies of how early Americans functioned during economic downturns, see Edward J. Balleisen, Navigating Failure: Bankruptcy and Commercial Society in Antebellum America (Chapel Hill, 2001), Peter J. Coleman, Debtors and Creditors in America: Insolvency, Imprisonment for Debt, and Bankruptcy, 1607-1900. (Madison, 1974), Bruce Mann, Republic of Debtors: Bankruptcy in the Age of American Independence (Cambridge, 2002), or Scott A. Sandage, Born Losers: A History of Failure in America (Cambridge, 2005).

For shifting expectations within the household, see Stephen M. Frank, Life with Father: Parenthood and Masculinity in the Nineteenth-Century American North (Baltimore, 1998), Shawn Johansen, Family Men: Middle-Class Fatherhood in Early Industrializing America (New York, 2001), Jack Larkin, The Reshaping of Everyday Life: 1790-1840 (New York, 1988), or Mary P. Ryan, Womanhood in America: From Colonial Times to the Present (New York, 1983).

Finally, to contrast the urban experience with rural America, see Joan M. Jensen, Loosening the Bonds: Mid-Atlantic Farm Women, 1750-1850 (New Haven, 1986), or Nancy Grey Osterud, Bonds of Community: The Lives of Farm Women in Nineteenth-Century New York (Ithaca, 1991).

This article originally appeared in issue 10.3 (April, 2010).

Sharon Ann Murphy is an associate professor of history at Providence College. Her first book, Investing in Life: Insurance in Antebellum America (forthcoming in 2010 from Johns Hopkins University Press) reflects her interests in the complex interactions between financial institutions and their clientele. She plans to focus her second book on the public relations problems of antebellum commercial banks.